Streaming Video Shift to Put Consumer–Not Content–First

Content Insider #771 – Fun Fades

By Andy Marken – andy@markencom.com

“What’s a bad miracle, they got a word for that?” – OJ Hayward, “Nope,” Universal, 2022

Okay, let’s get past the elephant in to room … Netflix lost a bunch of subscribers and expects to drop more in the quarters ahead.

They haven’t really done anything wrong; but in the past two years, the streaming (and entire content) industry has changed dramatically.

Hastings and several industry analysts had projected that there was going to be 1,636M SVOD global users in five years, spending about $70/mo. for their services.

That smelled like money … BIG money.

At the same time, there was a seismic shift in the rest of the content creation/production industry.

M&A activity and management changes hit every corner of the movie/TV industry with the old guard stepping aside – retired, fired or aligned to resign.

Of course, the new bosses with nosebleed salaries were going to produce miracles for shareholders and content creators because well, they were being paid tons of money so obviously, they were worth more than the folks they cast aside.

The new guys/gals knew they could shake up their organizations and not just dominate the theatrical and appointment TV but sweep over the techie streamer because they knew they could create the kind of movies/TV shows people everywhere would want to watch at home at almost any price.

Yeah … it was going to be that good!

Disney shifted, shook, changed–including upper, middle management.

Oh sure, there were a few of the old contracts but nothing a little money couldn’t resolve.

The phone guy shuffled things at Warner with the new team focusing on their new streaming service; but he found out content isn’t all fun and games so he made Discovery an offer they couldn’t refuse including a $43B debt.

Old content contracts caused a few issues but again, money talks.

Hulu had its people, priority changes as did Paramount, NBC/Peacock and just about every major movie/TV house around the globe.

About the only streaming houses that weren’t affected were the new kids on the block.

Sure, Netflix added Ted Sarandos as co-boss to help share some of the workload and blame with Hastings.

No one paid much attention when Bezos stepped aside to focus on his rocket company because Amazon Prime, IMDB TV (now Freevee) had other sources of income and SVOD/AVOD were just nice additions to their mix.

The content industry snickered when Apple brought out Apple TV+ with its slim library of old shows, low cost and promise for a rich content future.

Futball – Rather than rushing in with as much content as possible, Apple has followed its own path of creating and acquiring some of the best content available to build its movie/show library and audience. Shows like Ted Lasso resonate with their growing subscription base and their investors.

Of course, the content folks forgot that the company has a fan base of more than 1B device/app users worldwide who like to play in their well-furnished walled garden that produced more than $378B in revenue and profits of more than $152B plus in gross profit.

Then they grabbed a bunch of awards with their Ted Lasso series as well as great movies like Coda, Finch, Uncharted, The Banker, The Unbearable Weight of Massive Talent and Beastie Boys doc.

Sometimes, focusing on and listening to consumers pay off.

Individually, they’re all great but…

Too Much – Streaming your content directly to the consumer is a great idea, but people have reached the point where too much of a good thing is too much. Sanity, consolidation, common sense has to take place and only the strongest will survive.

There are just too **** many good subscription services, each with good to great content that people want to watch.

The other subscription services shouldn’t be (and hopefully aren’t) looking at the Netflix subscription drop with glee but rather like the canary in the coal mine.

Limits – As consumers struggle with day-to-day expenses, multiple streaming services become a luxury folks can’t afford so they add/drop services to meet their entertainment tastes and budgets.

According to recent research by KPMG, almost a third of folks have struggled to pay for all of their subscription services since the beginning of the year. Many folks are borrowing money or dipping into their savings to pay their bills just as services were increasing their monthly fees because of the “added value” of their content.

People have discovered they are paying the same (if not more) for their network connection/SVODs as they were paying for their old pay TV bundles as media companies pass their rising costs on to the consumers.

Priorities – Consumers shaved/cut their cable bundle to reduce their home entertainment budget and they’ll continue to add/subtract streaming services in the same way. The winners have to show real value in addition to making content selection fast and easy.

If it’s between paying increasing rent and higher food bills or sacrificing a streaming service or two, that seems to be a pretty easy choice.

In the past two years, SVOD services have focused their attention on the GenZ crowd (18-24) who were ready, willing and able to pay for more streaming/music services, often more than 2X the number of services and the more expensive services than older consumers.

But it appears that the “free ride” has come to an end as folks realize that too much of a good thing is … too much.

At the same time, they based their service price on the fact that they were going to continually refresh their offerings with new content that consumers absolutely, positively had to watch and at the service’s perceived value/price.

Sorry dude…

Dropped – There’s very little brand loyalty when it comes to adding/dropping streaming services as people focus on the movies/shows that keep them entertained and connected.

Churn has increased in the GenZ group because they have a comparatively lower disposable income and have much less brand loyalty than older subscribers.

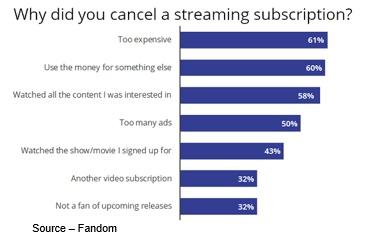

Over in Britain, research firm Kantar found more than 1.7M services were dropped at midyear, citing higher costs in other budget areas; and in the U.S., 57 percent of those surveyed got rid of three out of eight expensive services and also switched to less expensive options.

According to the KPMG study, over a fifth of the subscribers were willing to reduce the number of services they subscribed to and/or drop more expensive services for more economic alternatives or newer, smaller services–especially when they had more elegant user interfaces, better selection engines and more perceived value.

Surprise Winners – People are increasingly voting on which streaming services they will subscribe to based on personal taste and budget. In many cases, that works against the majors who overvalue their self-worth.

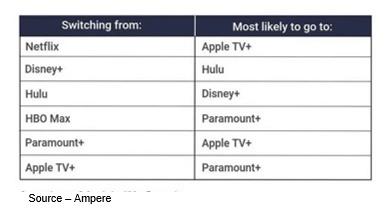

A recent study from Ampere Analysis found that Apple TV+ and Paramount + have been the most widely chosen platforms for SVOD switchers.

The churning streamers didn’t seem to add a new service to their huge bundle of streaming services but instead, transferred their spending while maintaining a core base of services.

At the same time, more than 50 percent of the folks said they were reducing their core SVOD services and adding ad-supported services such as Pluto TV, Tubi, Freevee, Peacock and YouTube as well as social media video options such as Facebook Watch, TikTok, Instagram and other social media video platforms.

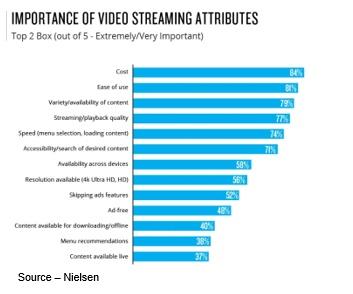

Ampere found that consumers are adjusting their home viewing service selection based on affordability (45 percent), a limited selection of titles (49 percent), lack of user -friendly interface (34 percent) and poor customer service (33 percent).

Both Omdia and Ampere have emphasized that while people are looking for ways to cut back on their streaming expenses, they still plan on watching the same or more hours of content through ad-supported services.

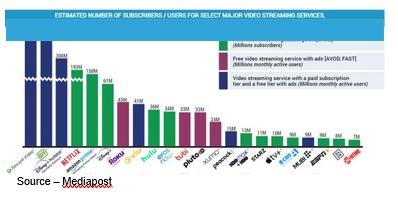

According to the services, more than 200M US consumers regularly watch AVOD services; and in Europe, 54 percent of streaming viewers are increasingly turning to ad-supported content.

Netflix continues to forge ahead to develop a rich roster of movie/TV franchises, spin-offs and show/movie extensions to maximize its ROI for their leading shows and movies in a similar fashion to what Disney has done so successfully.

At the same time, they are reluctantly rushing to build a lower-cost, ad-supported version of the service as has Disney, WBD and other services which were quick to follow Netflix subscription only example.

The minute Netflix, Disney+, Paramount+, HBO and the other golden subscription services announce their AVOD/FAST services, we’ll make the switch even though both Netflix and Disney have pre-announced that some of their content will be available only to SVOD customers.

Hub Entertainment Research found that 57 percent of those surveyed said they would tolerate ads and 26 percent reported that content matters more than ads.

Sure, there are those folks who say that ads are beneath them, and they’ll only watch subscription content, but people have a negative image of ads in their content because they’ve been abused … for years.

For crying out loud, the typical ad slot for yesterday’s pay TV was typically 20 minutes per hour.

It’s not whether consumers will accept ads with their content, it’s how they’re delivered.

Ads Ain’t Bad – Consumers have lived with ads – good/bad – for years, so the idea of trading off a little of their entertainment time to save money is once again becoming popular.

People are consumers … not targets.

With the volume of personal preference data available with IP-delivered entertainment, this is a chance for the content and ad industries to right the boat and deliver ads more efficiently and more effectively that people actually want to view.

Creating and pedaling ads is one of the things US services/marketers are really good at; and with a little bit of work and intelligence (okay, a lot), they could really make this thing work.

Folks like Netflix’ partner Microsoft, Disney’s Trade Desk, Peacock’s parent Comcast and ad verification specialists like Integral Ad Science can help develop ad platform opportunities that are contextual and more targeted ads that are less insulting, intrusive, and more interesting, informative and effective for the consumer.

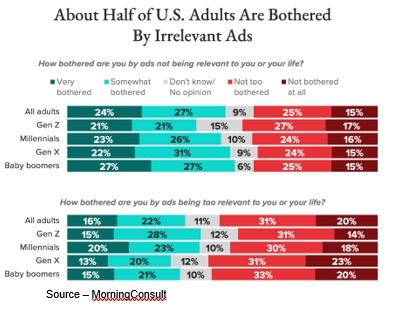

Balancing Act – With IP-based services, consumers don’t want to see ads that are completely irrelevant to them but at the same time, feel it’s creepy when they’re too relevant. Services and marketers need to strike a happy balance or folks will simply leave.

And it’s not that they have to do a lot of digging. All they have to do is set aside the idea that they know what consumers want … shut up and listen.

According to a Morning Consult survey, most folks say there are too many ads (44 percent), they are too repetitive (69 percent) and they’re too invasive (79 percent).

It should be pretty easy to limit the number of times we see the same ad in our household (IP address) because watching the same ambulance-chasing lawyer ad doesn’t make it more effective. Even multiple versions of the ad would be a relief!

Tubi, Freevee and Pluto TV are limiting themselves to three – five minutes of ads per hour with a range of pre-roll ads and/or ad block which is palatable as long as they’re not the same ads every hour.

The tough balance for streaming services is to deliver personalized (but not too personalized) ads that deliver the right message while respecting the viewer’s privacy … Yeah, it will take a little work.

There’s a fine line between being creepy and being effective.

Once streamers and marketers have a better understanding of what a targeted ad is, the better off we’ll all be.

Netflix, Disney, Hulu, Apple and a few other folks already have built up a sound base of trust with audiences.

Now all they have to do is continue to offer quality content and folks will spend time with the surrounding ads because it’s a reasonable value exchange.

That’s when the ad-supported services and advertisers will be able to high-five each other because as OJ Hayward said in Nope, “You know they’re gonna bring us back for the sequel.”

Services will make more (front and backend) than simply chasing more subscribers. Marketers will be more effective with their ads and folks will be able to watch content and ads they enjoy.

It may not be perfect, but our streaming video budget and family will be happier.

You only want ad-free content? Knock yourself out!

Andy Marken – andy@markencom.com – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software, and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.