Ads Get Better, More Welcome with Ad-Supported Services

Content Insider #911 – Intelligent

By Andy Marken – andy@markentcom.com

“For a tiny moment it felt good to have something to blame for all this, even if what he was blaming was the internet, which could never be made to care.” – Jackson Lamb, “Slow Horses,” Apple TV+, 2022

Home entertainment (formerly called TV) has changed and so has the advertising that has been jammed into it to reach, convince folks to buy … stuff.

The basic objective is still the same but how they get from point A to point B is different.

The Upfronts – where home entertainment services (networks/streamers) convince advertisers to invest in their audiences – have changed to being less dog and pony and more technical analysis.

Oh sure, there were still well-staged/rehearsed shows; but there was a lot more technical discussion and analysis of what the services are going to do to help advertisers educate, inform and entertain people without irritating the h*** out of them.

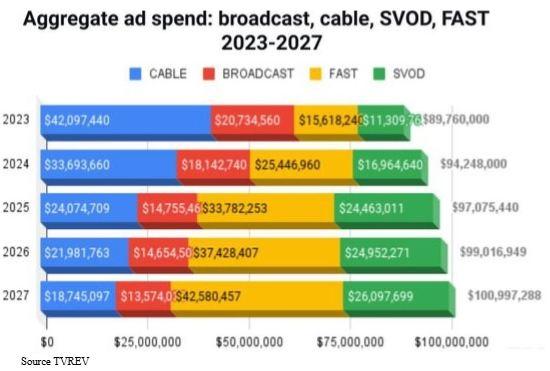

Yes, it’s big business because upfront TV advertising spending is expected to be nearly $170B globally this year and it’s becoming increasingly complex and creative.

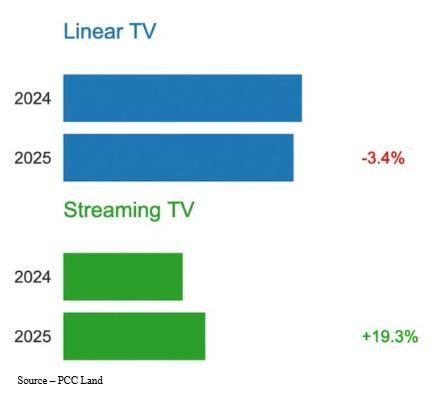

Ups, Downs – Pay TV continues to lose audience to streaming video services in the Americas while it continues to be stable in other countries, especially in emerging markets. But streaming services are winning new viewers everywhere.

The Upfronts were “invented” by linear TV people as a way to pre-sell the coming seasons of shows – and specific ad slots – to advertisers before the season began by doing what they do best … entertain their audience.

In this case, ad agencies and advertisers.

For example, last year late night host Jimmy Kimmel led off Disney Upfronts with a monologue to advertisers taking on almost everything and everyone including boss Bob Iger – https://tinyurl.com/mvshvnm6 And there was still humor and entertainment for the audiences this year when the Upfronts were segmented.

Linear TV has leaned heavily on the total volume of viewers (CPM) they service. However, streaming services and the ability to precisely compile data on the viewer, his/her preferences and activity make personalizing ads more efficient, more targeted and … more effective.

Linear TV will still capture the largest chunk of ad expenditures this year (72.6 percent) but the investment, like the audience size, is shrinking.

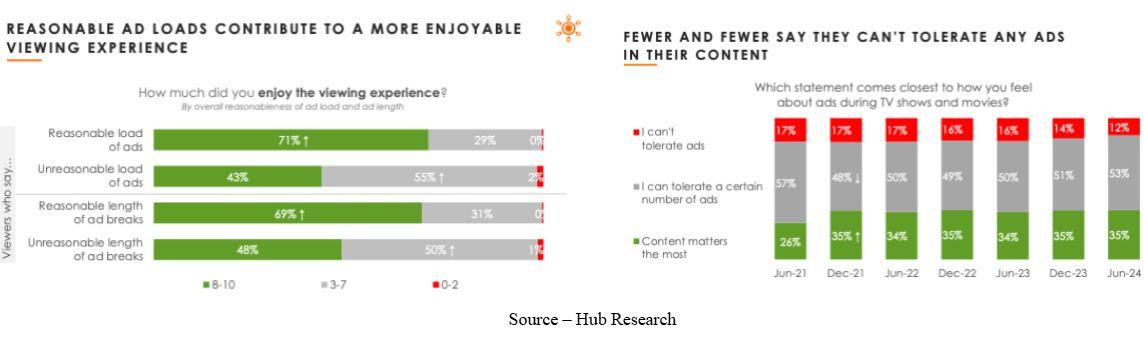

Pay TV carries 12-20 minutes of advertising per hour, compared to four-five minutes for streaming.

That was plenty of time for viewers to leave the room to take care of other stuff and sometimes even forget what the show was all about.

In addition to the higher volume of ads, TV users are also paying about $100/mo. for their entertainment bundle of 200 plus entertainment channels.

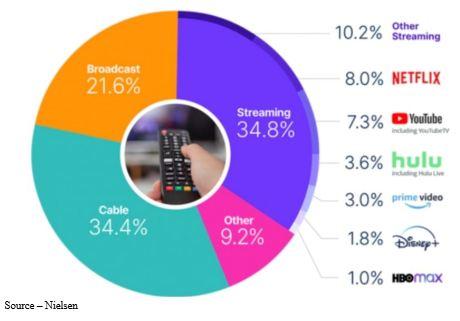

The pay TV/broadcast segment has been steadily losing audiences to streaming but still accounts for about 50M viewers in the US, primarily people who follow live performances and sports.

However, the global pay TV market will continue to grow, albeit at a much more modest rate.

Cable TV subscriptions are declining as most individuals and households opt for more flexible and more economic streaming services.

Netflix kicked off the streaming trend back in 2007, much to the bewilderment of networks and studios, and was certainly never imagined as a competitor to their money-making TV machines.

In fact, during the early years, they were more than willing to rent them their old shows and movies figuring: 1) who would want to watch the old stuff? and 2) hey it’s just another revenue stream.

They would, they did, and Netflix quickly moved to creating and buying their own shows/movies.

Other tech firms – Amazon, Apple – as well as studios/networks quickly followed suit and the entertainment market has become ad-free (of no interest to advertisers except to watch shows without interruption), ad-supported and free services (no fee, just ads).

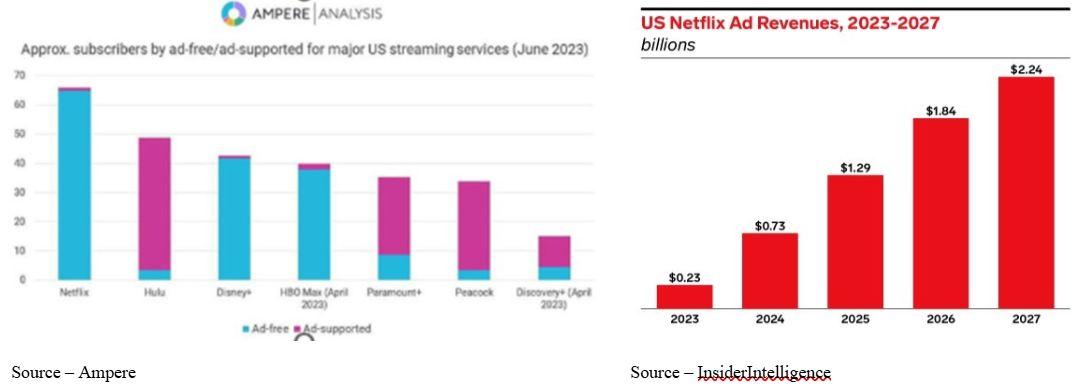

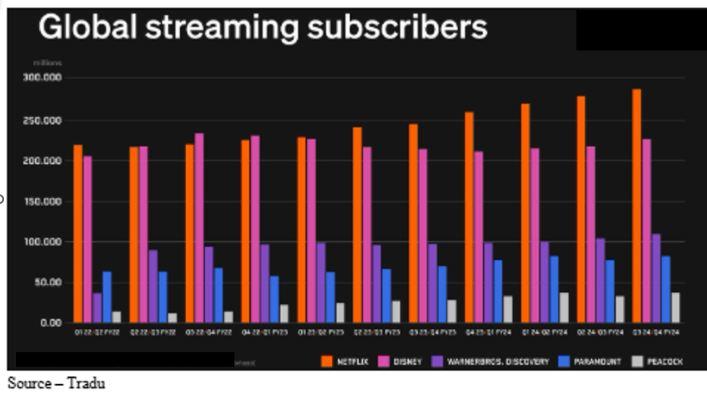

And the only streaming service making money was Netflix with nearly 283M subscribers worldwide.

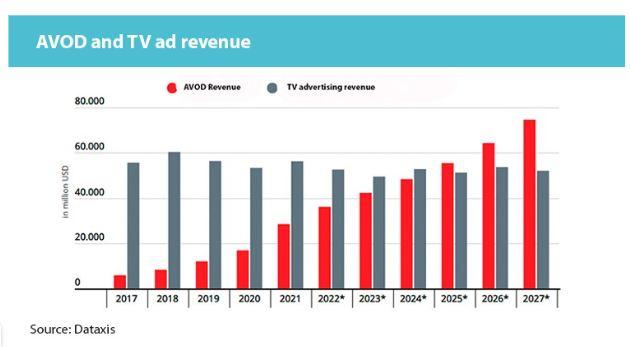

Disney and WBD finely turned red ink black this past year and they rolled out their AVOD offerings to help them capture more subscribers.

Today, with the exception of Applet TV+, all of the streaming services offer two flavors of streaming – subscription or ad-supported.

Budget Counts – With richer content options and less intrusive/abrasive ads, consumers seem to always opt for services based on their budget.

Yes, ads were added to their entertainment mix to improve their profits, but they were also – and perhaps more importantly – added to make their service options more inviting because of the lower monthly cost.

Actually, we somewhat enjoy ads.

After seeing the repeat of an ad 2x, we can repeat the punchline and even some of the dialogue.

Sorta’ reinforces to us that we don’t have dementia.

They also make us wonder why we’ve had to call an injury lawyer … guess we’re just not trying hard enough.

But we have friends who vehemently disagree with us when it comes to choosing between a subscription vs. ad-supported option on the services.

They swear to gawd they would never choose the less-expensive option given the choice.

That’s fine.

In fact, one of the individuals has his “free” subscription viewing down to a science.

He signs up for the free trial period – every service has ‘em.

He’ll binge all of the shows/movies he is interested in and just before the subscription kicks in, he drops them, moves on.

In six months if the service has a library of new “interesting” stuff, he’ll sign up for a new trial period, rinse and repeat.

It’s called churn and every service lives with the issue, including your wireless provider.

Services have learned to live with it – Wall Street hasn’t – and develops efforts, activities to keep people connected to them.

Netflix has done it by adding live shows, movies/shows from nearly all of the 190 countries where it has subscribers, video games and sports.

It works.

Netflix has what many refer to as insurmountable streaming services.

Late But – Netflix reluctantly entered the ad-supported arena late in the game but it’s entry also legitimized streaming advertising, especially when they developed an offering that didn’t simply throw ads into the content. The cautious – some say caring – approach also spells a rapid growth with subscriptions and financial returns.

Reed Hastings, Netflix chairman, vowed years ago that the streaming service would always be ad free, but he just proved … never say never.

The company is also a stellar example of how to offer a service that is good for the subscriber and advertiser.

Netflix has committed to serving up no more than four minutes of ads per hour to subscribers and at this year’s Upfronts, they said they would be working closely with advertisers to understand their advertising objectives.

In addition, they would assist advertisers in better understanding their subscribers so they could be more efficient and effective in reaching just the right viewers without irritating everyone else.

Balanced Satisfaction – Consumers, not entertainment services, determine what the right balance of ads/content are and when streamers meet the viewer’s expectations … everyone is happy.

Netflix and Disney (others are also working on improving their ad delivery) are implementing advanced subscriber analytics and ad delivery technologies that can create seamless, engaging and personalized ad experiences.

Disney enriched its advertising proposition for agencies and advertisers by bundling their stuff – Disney +, Hulu+, ESPN + and buying Fubo to double down on sports.

The bundle delivers a record 288M global subscribers and they have aggressive plans to continue their growth.

Rather than solely pitching “new shows and movie” opportunities at the Upfronts (yes, that was also there but…) they placed their emphasis on a large and stable content library supported by long-term licensing agreements to retain and attract subscribers.

Content is still king.

To benefit advertisers, they announced unique viewer first ad formats – which are being emulated – as well as a standard for transparency and measurement.

It paves the way for even better personalized ads for viewers as well as better reception/results for the advertiser.

With AI, advertisers are able to develop product feature/benefit modules so individualized/personalized ads are created and delivered in real-time–more efficiently and more effectively.

Admit it.

Aren’t you mildly curious as to what AI thinks will push your buy button?

We are!

Front Runners – Netflix and Disney presently lead the other streaming services in the number of subscribers by a large margin. Mergers or acquisitions seem to be a strong possibility for the other competitors.

Netflix and Disney have maintained and extended their leadership in global streaming with major emphasis on tying up as much of the live sports distribution as possible including football, baseball, basketball, soccer, cricket, boxing, hockey, tennis, you name it … including pickleball.

All of that activity also leads Wall Street to view the next 12 months with excitement because it can only pave the way for increased M&A activity as weaker service consolidation has to take place to remain competitive and profitable.

No one believes it will be a two-horse race and a couple of strong contenders will emerge from the pack in the months/years ahead.

Wind Change – The gala ad upfronts become less important to advertisers because gala show unveilings are less important than granual information on the audience and better ways to be more responsible/responsive to their target audiences.

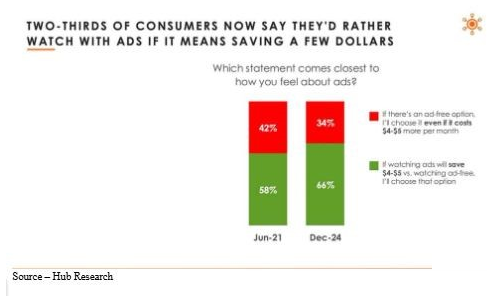

While ad-free streaming will remain the strongest segment, ad supported services will continue to grow because let’s face it, the monthly fee will go up, never down.

There will come a tipping point when everyone – except the most stubborn – will say that watching a few ads in an hour for lower out-of-pocket payments are worth the savings.

Especially when people see:

- The major services keep their commitment to maintaining the four-minute cap and instead share their cost increases with advertisers who can more efficiently/effectively zero in on specific, interested viewers.

- Viewers and advertisers realize that the ads aren’t intrusive but rather interesting because they attract real potential product/service buyers.

Advertisers will embrace them because:

- They ensure ads will appear within/around content that will not damage the company’s/product’s reputation.

- The ads are accurate, viewable and measurable.

- Advertisers have a better understanding/visibility on the total selection/delivery process and can accurately measure results.

Okay, we’ll admit it, the minute our major streamers added an ad-supported option to the mix, we signed up.

Disney – check

Netflix – check

Amazon – have you seen how they simply throw in a bunch of ads? Except for wife’s delivery – nope

YouTube – Ah, no!

Apple TV + – no, no ad-supported tier but daughter has “gotta” have Apple One (small check mark)

Peacock, Paramount – we’ll wait and see.

But we and tens of thousands of people around the globe are a long way from being entertainment deprived.

FAST services are attracting audiences because they prioritize free access, variety and non-intrusive ads.

It has taken services like Pluto and Tubi a long time to gain audience interest and trust.

Adding features like tailored user profile, adaptive UIs based on viewing behavior, interactive options such as story voting and customized viewing make viewers, especially Gen Z feel as though they’re heard and understood.

FAST services have increased their audiences with Horowitz Research finding that 66 percent of US viewers use them every month. Kantar reports that the audiences are growing at three percent per month, which is slightly higher than subscription services.

FAST is Fast – Really free streaming services are rapidly growing by offering viewers a greater range of viewing options to meet the broad marketplace’s interests and tastes. Obviously, advertisers want to be where the audience is.

The services benefit because content creators/owners want to monetize legacy, niche libraries.

In addition, they are taking pages from subscription services’ playbook by inviting and revenue sharing with original projects as well as cautious entry into live sports, especially localized and niche activities.

The rapid audience growth and diversity is especially attractive to advertisers, especially local and regional advertisers as well as retail and specialty product/service providers that can hone their messages for very specific audiences because of a granular-viewing market that can now be used.

The viewing numbers may never be as large as Netflix and Disney regularly hype for their movies/shows; but convenience, variety, personalization and measurable results will increase their popularity with viewers … and advertisers.

As Jackson Lamb said in Slow Horses, “We’re All Targets. Just Like Old Times.”

Actually, it’s better than old times because what the content people want is available when they want and on the screen they want to use, the ads are fewer, less intrusive and more informative, educational and just better.

We have to admit that we’re going to miss all those accident lawyers and fast-food ads … not!

Andy Marken – andy@markencom.com – is an author of more than 800 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software and applications. Internationally recognized marketing/communications consultant with a broad range of technical and industry expertise, especially in storage, storage management and film/video production fields. Extended range of relationships with business, industry trade press, online media and industry analysts/consultants.