Streaming Emboldens Consumers and Creators

Content Insider #740 – Service Shift

By Andy Marken, andy@markencom.com

“Now, they’ve been here before, so they’re not gonna give it to us! We gotta go out there and we gotta take it!” – Coach Don Haskins, “Glory Road,” Disney, 2006

A while back, we read an article on the top 10 best brands of 2021 in the U.S. according to consumers.

Three of the top 10 were entertainment folks – Netflix, Amazon, Apple.

Where were the rest?

- Disney – 13

- HBO – 60

- YouTube – 75

Who’s missing?

Warner, NBC Universal (Peacock), ViacomCBS (Paramount +) , Comcast, Charter.

And, of course, that doesn’t include leading EMEA and Asian pay/streaming entertainment services that have a major impact on what/when/where people watch their content.

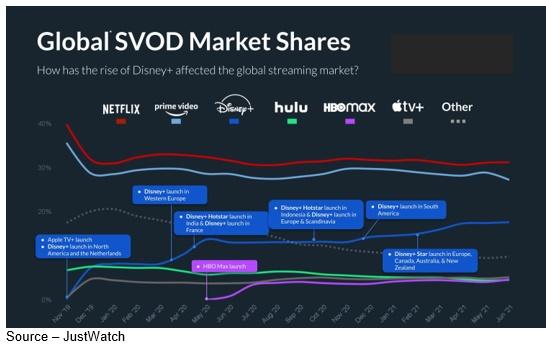

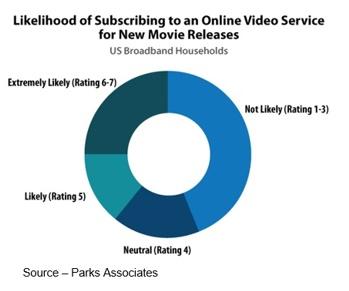

So, what do all the reports from JustWatch, Parks Associates, Parrot, and the other M&E research folks have on who’s winning the streaming battle mean?

Think About It

It means people have a couple of regulars that they go to regularly for their entertainment and then a few others when they simply go to their screen to watch … something.

It also means the missing brands – and they are brands, not just one good show after another – are spending so much time looking at the numbers of the other guys they forget what those numbers mean … people, subscribers!

Yeah, we know the Hollywood adage – content is king – but this isn’t precisely true.

Share Growth – If you don’t have to deal with the issues/challenges of content delivery of yesterday, it’s a lot easier for streaming services to grow quickly. Of course, it doesn’t hurt to have a global positive image either.

Mindshare and distribution are an important part of the streaming world.

Streaming changed entertainment’s ground rules.

Now when a person wants to watch something, they don’t simply scroll down a day/time program list, they move from app to app.

That’s work!

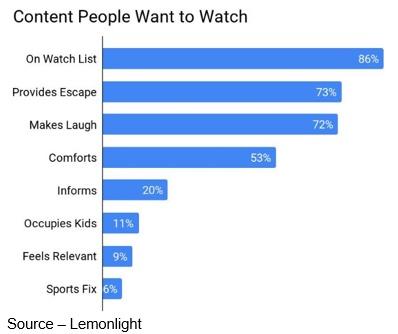

To simplify things for people, the service’s recommendation engine suggest content you’ll probably be interested in because of what you’ve watched in the past.

Next – To keep subscribers, SVOD services have sharply honed their recommendation engines to understand what you have previously watched and what you will likely want to view now. For most folks, that’s good enough.

Or, if you’re a snobbish cinephile, you can tell us you researched for hours – checking out Rotten Tomatoes, JustWatch, Reelgood, THR (The Hollywood Reporter) and all of the streaming recommendation apps – to make an informed decision.

Yeah, like folks believe you.

Whether it’s a movie or TV show, it’s just not the way the entertainment industry runs today, and studios/streaming services know it.

The key is hooking a consumer/subscriber and keeping them entertained with your shows/movies as long as possible using a healthy dose of emotional appeal and technology.

Disney, Netflix, Amazon and yes, even Apple, know it.

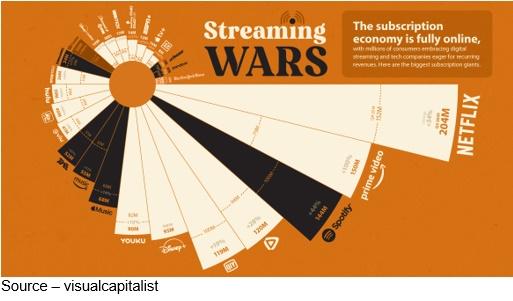

The best example of emotion and technology is arguably Apple with the products and apps folks use around the globe – 100M Mac users, 1B iPhone users, 2.22M apps including Apple TV+ with 660M total subscribers and a modest but growing library of attractive games/apps/music/publications/movies/shows.

The world’s online shopping store, Amazon has 300M active accounts and 150M paid Prime members who watch something in between purchases.

Netflix, the red envelope folks who upset the “normal” entertainment industry, has more than 200M subscribers in 190 plus countries with a constant flow of new global projects that keep people coming back to watch their favorites and new stuff.

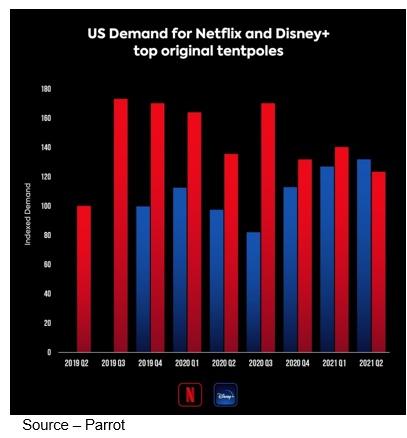

Differences – Netflix and increasingly, all streaming services are using their customer inputs to develop films/shows that will resonate with the broadest number of people. Then they promote them to their subscribers in the ways that will capture their attention.

Their exhaustive database of what resonates with people everywhere – and for how long – helps them pick projects folks will probably want to watch and gives creatives a boost on what visual stories that should resonate with audiences and award judges.

Yes, awards are important because the social media noise attracts subscribers.

That same social media noise, as well as their subscriber analytics and viewing entertainment in its total context and not just video also stimulated them to begin adding gaming/games to their entertainment roster.

Games have proven to provide stickiness for Apple, Amazon and their large/often overlooked competitor — Google/YouTube – especially on a global scale.

Connected Profit – Netflix couldn’t help but notice that game play on Amazon and Apple had global appeal with people and that they stayed with their games for a long time if they were continually refreshed in a quality manner.

According to a recent Limelight State of Online Gaming Report, https://tinyurl.com/47mdncxz, the time spent and the number of people around the globe increased 14 percent, meaning it is increasingly a part folks’ everyday life.

But when it comes to entertainment for entertainment’s sake, Disney is often viewed as the gold standard in creating, monetizing projects.

In the past two years, it has shown folks it’s a quick learner when it comes to the new entertainment space.

Shifted Focus – While Disney has “always” been the go-to studio with big hits for theater owners, the nearly 18 months of shutdown made the company rethink its content delivery to people around the globe to using modified theatrical windows or straight to streaming. It’s nothing personal, just business. The shift attracted new subscribers … rapidly.

The “normal” path for Disney’s – and every studio’s – projects around the globe was thrown in complete disarray.

They responded as best they could given the fluid environment they were operating in at the time, making no one completely happy except entertainment-hungry folks.

They maintained strong M&A (marketing & advertising) pushes including partnerships with major companies, tie-ins with toys, social media feeds and a flexible release schedule based on the investment in the project and the ever-changing consumer environments.

Consumers who “had to” see a major film in a theater put seats in seats whether it was a 45-day window or day/date release.

About the Same – The desire to see a movie in a movie theater first hasn’t dropped dramatically. People who still have to enjoy a film as it was created to be shown will still put seats in seats while others have … options.

There are people – a lot of people – who simply can’t enjoy/appreciate a film unless they see it in a darkened room with a bunch of strangers on a huge screen with Dolby Atmos sound while sitting in a cushy lounge seat with their drink and popcorn close at hand.

There are people who will wait quite a while before they take their unvaccinated kids to enjoy the video story.

There are folks who can’t remember when the last time they saw something at the cinema because watching it at home was easier and enjoyable, especially with their huge screen, surround sound and favorite recliner.

Some individuals will wait until they get their DVD set so they can enjoy their film and dissect every portion of the project.

Youngsters raised with a screen in their hand are perfectly happy streaming the show to their iPhone with decent audio.

Unfortunately, there’s even a segment of the population who can’t really enjoy a film/show unless it’s “free.”

They like it more when they download it from a Torrent site or borrow someone’s password.

Don’t kid yourself, there’s no line item for them on the M&A budget.

Even as the halcyon days of the global box office is past, the shift from theatrical to broadcast/cable to streaming isn’t easy for studios or streamers.

Growing Pile – As film distribution options have grown (theatrical, airline, pay TV, discs, national/international, streaming) so has the complexity of contracts. It’s a situation only a lawyer would love.

Just ask Disney’s and Scarlett Johanssen’s lawyers. Or Warner’s legal team when Jason Kilar bravely said the company was going to throw all its 2021 slate onto HBO Max and big screens wherever possible.

AT&T’s John Stankey sidestepped the issue by doing a deal with Discovery’s David Zaslav to take over the rich Warner Bros assets and let the respected M&E industry veteran turn it all into a global entertainment entity.

But straddling the full spectrum of video story distribution is complicated because license fees, key member upfront/backend payments, episodic orders and financial models for each distribution venue, various country distribution guidelines/fees and aftermarket potential/fees, as well as hundreds of agents and lawyers.

Netflix minimized the quagmire by paying higher project front ends whenever possible to more effectively control their use/distribution of content.

Tech, Internet born competitors followed suit while studios and networks worked through their new “opportunities.”

Pay TV is no longer the tool for mass reach.

Fight for Viewers – Tech and social media sites quickly recognized that people around the globe were going to spend hours online to be entertained. Streaming video has quickly become a huge and complex business.

Connectivity and the growing streaming video options have also shown that racial, ethnic and sexual identity/orientation are important and more easily/more economically addressed and appealed to with tailored content and marketing.

Knowing who is watching what and for how long is becoming increasingly critical for streaming services and, in the case of AVOD services, vital for brands.

Creating content that resonates with specific audiences – especially those that have been historically excluded with pay TV – has become an important part of the strategy for streaming services to win and retain viewers.

It could also mean that much of the studio’s/network’s “high value” library needs to be repurposed to appeal to the new audience(s) or forever retired.

High-profile originals will attract new subscribers, but exclusive content keeps people regularly involved and reduces churn.

Global streaming service winners will have to adopt a lot of new guidelines and be more flexible/reasonable in their dealings with content creation partners.

Everyone in the new entertainment environment also must understand their value in the changing M&E world and remember what Coach Don Haskins said, “Nobody can take something away from you you don’t give them.”

Being granted a slot on the Cineplex/AMC calendar is becoming far less important in reaching today’s global audience.

There are new, perhaps even better, ways for content creators and consumers to connect.

Andy Marken – andy@markencom.com – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software, and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.